SBA Loan Crisis Ahead? Project 2025 Workforce Cuts Spark Concern for Small Businesses

By Morgan Everett

In a sweeping effort known as Project 2025, conservative organizations—including the influential Heritage Foundation—seek to profoundly reshape the U.S. executive branch, with severe implications for federal agency staffing. At the core of this initiative is a push to “dismantle the administrative state,” a phrase echoed repeatedly by its proponents, suggesting extensive cuts to government employment and services.

One of the most immediate concerns centers around the Small Business Administration (SBA), an agency vital to American entrepreneurship. Under the planned reductions, the SBA anticipates losing approximately 43% of its workforce, sparking fears among lenders and small business advocates of significant delays in loan processing.

“There’s no doubt these cuts will extend processing times,” said Sarah DeMarco, a financial consultant who regularly works with SBA-backed loans. “We saw this during government shutdowns—reduced staffing equals longer waits.”

Project 2025, which traces its roots to former Trump administration officials and influential conservative groups, explicitly outlines an aggressive shift in staffing priorities. Civil service positions traditionally insulated from political shifts could replace their occupants with individuals loyal to specific political agendas. Critics worry that this shift could reduce bureaucratic accountability and threaten the quality of public services.

“Replacing seasoned career professionals with politically loyal appointees could severely impact efficiency and transparency,” warned Emily Torres, a senior policy analyst at Democracy Forward, who describes Project 2025 as an existential threat to governmental checks and balances.

The Department of Government Efficiency (DOGE), a new agency spearheading these cuts, operates under explicit orders to implement drastic workforce reductions. A stringent “one-in, four-out” hiring policy allows agencies to hire only one new employee for every four who exit. Diversity, equity, and inclusion initiatives, alongside other non-legislatively mandated programs, are primary targets for elimination.

“DOGE is aggressively pursuing its mandate,” confirmed an administration official speaking under the condition of anonymity. “Every agency is feeling these changes, not just the SBA.”

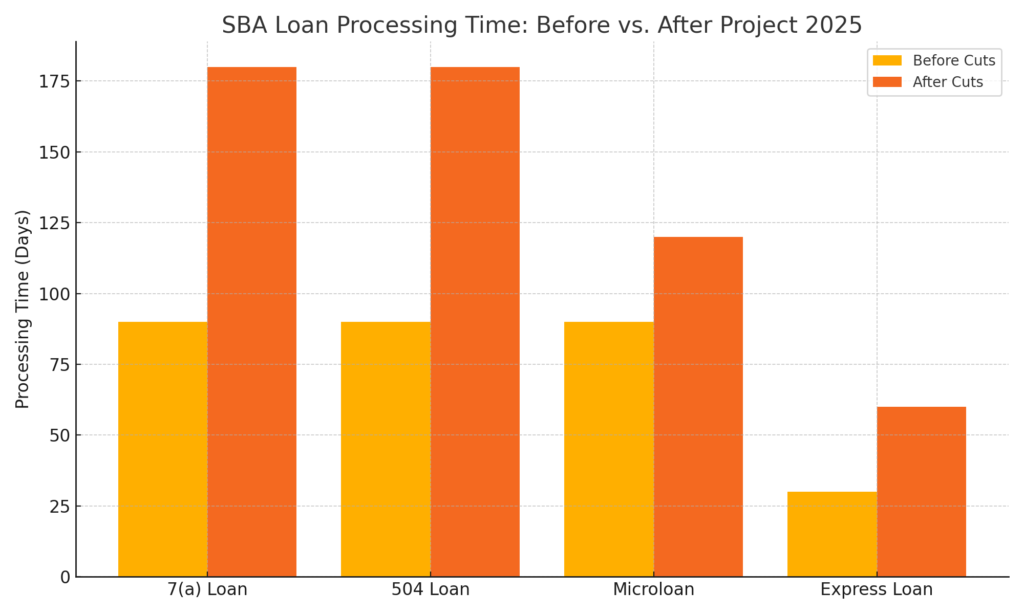

The SBA processes loans through a multi-step mechanism involving loan applications, underwriting, approval, and disbursement. Typical processing timelines for flagship programs such as 7(a) loans average around 60-90 days, with some extending considerably longer. Lenders predict that workforce reductions on the scale proposed by Project 2025 could nearly double these wait times, particularly affecting complex loans like those within the SBA’s 504 program, which sometimes take up to six months.

“We’re already stretched thin,” explained Michael O’Brien, a loan officer specializing in SBA programs. “Almost halving the staff will amplify existing issues. Small businesses can’t afford to wait months for capital.”

James Bryant, owner of Bryant’s Café in Chicago, shared his concerns firsthand. “During COVID, SBA loans were lifelines. Imagining even longer waits terrifies me—our entire community relies on prompt funding.”

Experts emphasize automation’s limitations while the SBA pledges to offset staff losses through technological enhancements, utilizing automation for data entry, preliminary document checks, and initial underwriting.

“Technology is helpful, but human judgment and personalized service remain critical,” noted DeMarco. “Many business cases are nuanced and require individual attention that a machine can’t provide.”

Adding complexity, the SBA faces additional challenges from the planned transfer of the Department of Education’s massive student loan portfolio. This responsibility and reduced staffing raise serious doubts about the SBA’s capacity to deliver timely and effective services.

“The cuts and additional duties seem contradictory,” says Lloyd Chapman, president of the American Small Business League. “They’re setting up the SBA for failure.”

These anticipated delays carry broader economic implications, particularly for minority-owned and underserved businesses, which disproportionately rely on SBA financing. Small companies, historically significant job creators, could face critical funding gaps, forcing them toward costlier alternatives and thereby hindering community economic development and innovation.

Experts suggest businesses prepare by exploring alternative funding sources and building financial resilience. “Businesses should proactively identify backup lending options,” advises DeMarco. “Being prepared might lessen the blow.”

“When small businesses thrive, communities thrive,” emphasized DeMarco. “Delays and inefficiencies from these cuts could ripple negatively across the entire economy.”

As Project 2025 unfolds, tensions persist between its architects’ drive for government efficiency and advocates’ concerns about small business health. While SBA leadership maintains optimism about its restructuring plans, small business advocates and financial experts warn that, without significant adjustments, the U.S. economy’s backbone—small businesses—could suffer lasting impacts.